from CoTec Holdings Corp. (CVE:CTH)

CoTec Announces Updated Mineral Resource and Positive Preliminary Economic Assessment for the Lac Jeannine Iron Tailings Project, Québec, Canada

VANCOUVER, BC / ACCESS Newswire / May 20, 2026 / CoTec Holdings Corp. (TSXV:CTH)(OTCQB:CTHCF) ("CoTec" or the "Company") is pleased to announce an updated independent Preliminary Economic Assessment ("2026 PEA") for the Lac Jeannine Iron Tailings Project, Québec, Canada ("Lac Jeannine", or the "Project") which includes a new Mineral Resource Estimate (the "2026 MRE") that was developed following the August 2025 drilling programi and is consistent with the previous PEA and Technical Report filed in 2024 ("2024 PEA").ii

The 2026 MRE was prepared byMinéralis Consulting Services ("Minéralis") and the 2026 PEA by independent experts Addison Mining Services Ltd., Axe Mining Solutions Limited, Soutex Inc, JPL GeoServices Inc. and other independent experts.

The highlights of the 2026 MRE and 2026 PEA are as follows:

A 41% increase in the resource compared to the 2024 PEA with a global increase in Total Fe grade from 6.7 to 6.8 %FeT.

Category

2024 PEA

2026 PEA

Tonnage (Mt)

Total Fe (%)

Total Fe (Mt Metal)

Tonnage (Mt)

Total Fe (%)

Total Fe (Mt Metal)

Indicated

0

0.0

31

6.82

2.1

Inferred

73

6.70

4.9

71

6.80

4.9

(Note: tonnes are metric tonnes, see below for MRE notes)

Conversion of 31 Mt of inferred resource into indicated resourced supporting the first four years of production.

The 2026 MRE has resulted in extension of the life of mine to 15 years from 11 years with total tonnes of concentrate produced increasing from 3.8 Mt to 5.4 Mt.

Following a trade-off study, the proposed mining method has been changed from contract mining, (using trucks and front-end loaders) to a continuous miner with overland conveyors. Capital expenditure ("CAPEX") for the continuous miner is estimated to be US$6.8M with an operating expense ("OPEX") of US$0.65/t mined.

Based on open-pit extraction methods and the production of a gravity concentrate via conventional processing techniques and at a discount rate of 7.0% (and based solely on the 2026 MRE), the pre-tax NPV is US$141.5M, and its IRR is 33.8%, and the after tax NPV is US$91.9M, and its IRR is 29.6% with payback achieved in 2.3 years and a profitability index (PI) of 1.2.iii The after tax NPV does not include any potential benefit from government incentives, tax or otherwise.

The product remains a high purity iron concentrate at 66.8% FeT, low contaminant SiO2, Al2O3 and phosphorus with an average production of circa 360kt per annum for 15 years.

The up-front capital cost is US$69.4M which has increased marginally from the 2024 PEA figure due to the change in mining method.

C1 cash costs have decreased to US$46.8/t from the 2024 PEA level of US$53/t (excl. transport to port and royalty payments); this is due to the change in reclamation method which decreased the cost from US$0.9/t mined to US$0.65/t mined and a re-basing of G&A costs from US$0.3/t mined to US$0.25/t mined, which is more in line with other operators in the region with updated input costs.

All-in Sustaining Cost (ASIC) is US$54.5/t compared to the 2024 PEA figure of US$61/t (incl. transport to port and royalty payments).

The 2026 PEA does not include further tailings that are present outside of the indicated and inferred drilling area of the 2025 drilling campaign and further potential upside from the application of the Salter gravity separation technology that would allow access to the ultra-fine material contained in the tailings.

Julian Treger, CoTec CEO commented; "the updated PEA is a very important step forward for the project as we continue to work through the Bankable Feasibility Study. Achieving 103 million tonnes of mineralized material increases the life of mine to 15 years. This improves the long-term economic opportunity the project offers, not only to CoTec but to the surrounding communities and stakeholders.

In partnership with BBA Consulting of Montreal, CoTec have made significant progress on the project and identified a clear path forward to deliver the Bankable Feasibility Study and obtain the required environmental permits for the project. Through our discussions with our stakeholders, we continue to receive positive support as the Company progresses through the environment baseline studies.

The further optimization work, inclusion of the remaining 28 million tonnes to 40 million tonnes of exploration material and application of the Salter gravity separation technology could potentially add further significant upside. We will also be investigating possible ways to upgrade the FeT content of the concentrate from the current level of 66.8% to 67% iron concentrate suitable for direct reduction iron (DRI) production, which is crucial for green steel production."

Details of 2026 PEA

The 2026 PEA study was undertaken by a multidisciplinary team appointed by CoTec and supported by Minéralis Consulting Services Inc, Axe Valley Mining Consultants Ltd, JPL GeoServices Inc, Amerston Consulting Ltd. and Addison Mining Services Ltd. of the United Kingdom. No changes were made to the process flowsheet; Soutex were not required to update sections 13 and 17 of the 2024 PEA so those sections remain unchanged in the 2026 PEA. A Technical Report for the Project, including the details of the 2026 MRE and its 2026 PEA, will be filed on https://www.sedarplus.ca/ within 45 days.

The key financial and production metrics of the Project are summarized in Table 1. The 2026 PEA did not incorporate prospects for potential economic support from governments, funding opportunities or other economic incentives that could improve economics and influence a future feasibility study ("FS") and investment decision, including those aiming to encourage the development of critical minerals and a circular economy.

Table 1: 2026 PEA Key Financial Metrics in US$

Assumptions | Unit | |

Mineralized Material | M dmt | 103 |

Project Duration | Years | 15 |

Average annual production (dry) | K tonnes per annum | 360 |

Average FeT In-situ grade to plant | % | 6.8 |

Average FeT metallurgical recovery | % | 51.6 |

Average concentrate grade sold | % Fe | 66.8 |

Economic Assumptionsiv | ||

P65 Index CFR China Iron ore price | US$/dmt | 121 |

Average realised price (Inc. high grade premium) | US$/dmt | 145 |

Average shipping cost | US$/dmt | 21 |

Capital Cost | ||

Construction period | Years | 2 |

Initial CAPEX (excl. closure, study costs and sustaining) | US$ million | 69.4 |

Operating cost per tonne | ||

Total cash cost (C1 Cost) | US$/dmt | 46.8 |

Total AISC | US$/dmt | 54.5 |

The 2026 PEA is preliminary in nature and is based on a combination of Indicated and Inferred Mineral Resources. Inferred Mineral Resources are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as Mineral Reserves. As such, there may be no certainty that the 2026 PEA will be realized.

Basis of 2026 MRE

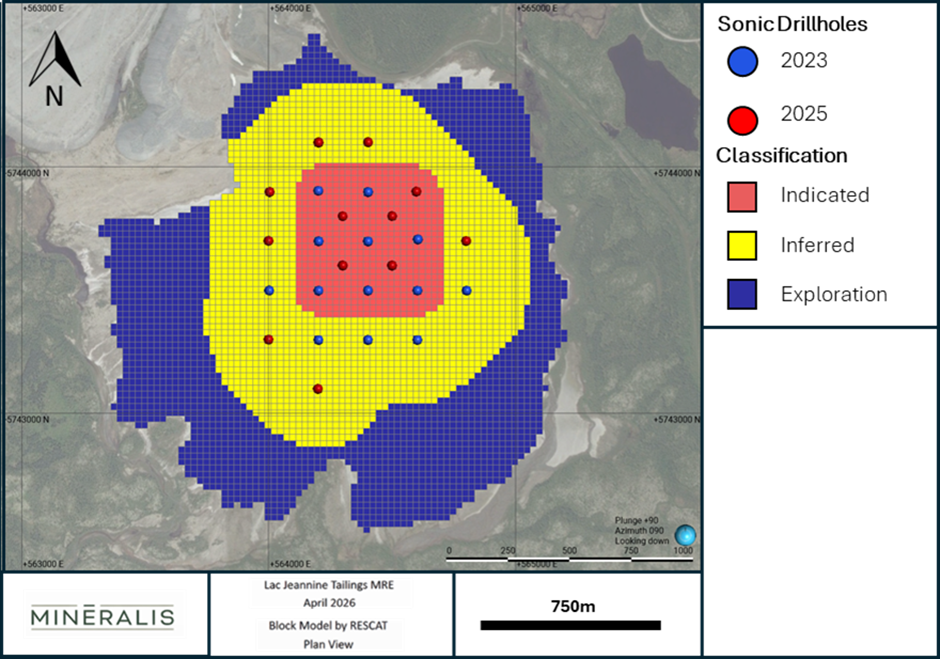

The MRE is based upon 25 sonic drillholes totalling 1,083 m (ranging between 36.0 m and 57.9 m in depth). All drillholes were drilled vertically and spaced from 100 m to 200 m apart on a regular staggered grid. The internal tube diameter was 4.05 inches. All material was logged for colour and grainsize characteristics, the average drillhole recovery was estimated at 93%. Routine quality control samples were inserted into the sample stream representing 85 out of 698 samples typically of length 1.5 m. Drilling and sampling was directly supervised by Mr John Langton (P.Geo.), Independent Qualified Person for Exploration, Drilling and Data Collection, in September of 2023 and August of 2025.

All drillhole material, minus a small 1.0 to 1.5 litre reference sample were dispatched in clearly labelled bags with sample tickets to Corem, a Québec City-based laboratory for analysis. Corem is internationally accredited by the Canadian Standards Council through the Bureau de Normalization du Québec (BNQ) to ISO/IEC 17025:2017 Analytical Services Laboratory.

All material was recorded upon receipt, and weighed wet and after oven drying. Sub sampling was done by rotary sample splitter before pulverization and preparation of a tungsten fusion bead for XRF analysis of major oxides (SiOâ, AlâOâ, FeâOâ, MgO, CaO, NaâO, KâO, TiOâ, MnO, PâOâ , CrâOâ, VâOâ , ZrOâ, and ZnO) plus Loss on Ignition.

Mineral Resource Statement

Mineral Resources, reported in accordance with National Instrument 43-101, Standards of Disclosure for Mineral Projects, ("NI 43-101") and prepared under Canadian Institute of Mining, Metallurgy and Petroleum ("CIM") Definition Standards, have been estimated for the Project. The MRE is reported inside an optimized open pit shell to respect Reasonable Prospect of Eventual Economic Extraction (RPEEE) and is supported by the 2026 PEA.

The estimated 2026 MRE, reported in accordance with NI 43-101 and the CIM Definition Standards is set out in Table 2 and the accompanying notes for further information and Figure 1 for an overview of the 2026 MRE:

Indicated Mineral Resources of 31 Mt at 6.82% FeT for 2.1 Mt of contained FeT.

Inferred Mineral Resources of 71 Mt at 6.80% FeT for 4.9 Mt of contained FeT.

Table 2: 2026 Mineral Resource Estimate

Category | Million Tonnes | FeT grade % | FeT (Mt) | Fe2O3% |

Indicated | 31 | 6.82 | 2.1 | 9.76 |

Inferred | 71 | 6.80 | 4.9 | 9.73 |

Notes To 2026 MRE:

Numbers are rounded to reflect that an estimate of tonnage and grade has been made, as such products may have discrepancies. Tonnages are expressed in the metric system and metal content as percentages.

The Independent Qualified Person for Mineral Resources, Mr Christian Beaulieu, P.Geo., is a member of l'Ordre des géologues du Québec (#1072). Mr Beaulieu has reviewed the available geological, assay and quality control data and has completed a site visit on the 7th of August 2025. Mr Beaulieu has been an employee of Mineralis Consulting Services Inc. since the 1st of June 2023.

The effective date of the 2026 MRE is the 23th of March 2026.

These Mineral Resources are not Mineral Reserves as they do not have demonstrated economic viability. The quantity and grade of reported Inferred Resources in the 2026 MRE are uncertain in nature. It is reasonably expected that the majority of Inferred Mineral Resources could be upgraded to Indicated Mineral Resources with continued exploration. No Measured Mineral Resources are reported.

The estimate was completed using Leapfrog Edge 2025.3.1 software, a 25 m (east and west) by 3 m (vertical) regular block model was estimated using ordinary kriging of all elements analyzed. The block model was restricted using a wireframe volume generated from airborne drone topographic survey of the current tailings surface, a legacy 1:50k contour map of the pre-tailings situation and bedrock information encountered in drilling.

Drilling reached the bottom of the tailings in seven (7) drillholes and the resource was extrapolated ~10 m below the drillholes that did not reach the bottom.

The cut-off grade used to report the 2026 MRE is 3.4% FeT, based on the following parameters:

Iron price of US$ 124/t FOB for a 66.8% Fe concentrate

Transport costs all in of US$ 6.32/t conc.

Total ROM-based costs of US$ 2.46 /t conc

Metallurgical recoveries of 51.56%

Royalties of 0.5%

No dilution and no mining loss were assumed.

Bulk dry density is assumed to be 1.78 g/cm3 across all tailing material. The density assumption is supported by on-site bulk density measurements and corrected for humidity content.

The Mineral Resource extends from surface to approximately 55 m below surface, it is laterally extensive over an area of approximately 1.25 km from east to west, 1.40 km from north to south and is extrapolated approximately 250 m beyond the limit of the drilling.

CIM Definition Standards for Mineral Resources (2014) and Best Practices Guidelines outline by CIM (2019) have been followed.

The independent Qualified Person for the mineral resource estimate is not aware of any known environmental, permitting, legal, title, taxation, socioâpolitical, marketing, or other relevant factors that would materially affect the estimate. Mineral resource estimates remain subject to inherent risks and uncertainties, and future factors could materially affect the estimate.

Figure 1: Extents of Mineral Resource relative to drilling and Exploration Target

Exploration Potential

Further tailings are present outside of the drilled area and it is reasonable to expect that with further appropriate exploration drilling the 2026 MRE tonnage could be increased. The surveyed area of the tailings has a total estimated tonnage of 145 million tonnes. This tonnage is likely estimated to relatively close limits (±5 million tonnes); however, iron grades are unknown with only limited sampling of the surface having been completed outside of the drill tested area; not all material may have a reasonable prospect of eventual economic extraction should grades be below economic cut-off, mixed with other waste material or contain significant quantities of deleterious elements.

A study completed by Soutex in 2007v postulated that 154 million tonnes of tailings grading 7.5% FeT were deposited at the Lac Jeannine tailings pile. Soutex's estimate was based on historical production and mass balance records rather than systematic sampling. The results are similar to the findings of this study albeit at a slightly higher grade.

Assuming 70% to 100% of the tailing's material surrounding the Inferred Resource has a similar FeT grade to the 2026 MRE, an exploration target tonnage of 28 Mt to 40 Mt is postulated, with global average FeT grade of 5.9% to 7.7% (±1 SD of the Resource block model) considered a reasonable possibility.

This potential range of tonnes and grade is conceptual in nature. Insufficient exploration to define a Mineral Resource has been completed and it is uncertain if a calculated mineral resource estimate of the surrounding material will be made in the future.

Basis of Preliminary Economic Assessment

Scoping-level design and preliminary economic analysis thereof was undertaken for the Project. The 2026 MRE has been used as a basis for the 2026 PEA.

Mining via open pit methods using a continuous miner and overland conveyor transporter, delivering approximately 7 Mtpa of Run of Mine ("ROM") to stockpile for processing. On site mineral processing is via screening and size classification followed by gravity separation to produce a bulk iron bearing concentrate for sale. Rejected waste material from mineral processing is expected to be disposed of in the legacy Lac Jeannine open pit allowing rehabilitation of the mined parts of the current tailings pile. Preliminary economic analysis has been performed in accordance with the conceptual mine design and schedule, metallurgical testing, and concentrate payability analysis developed in the study, and the estimates and analyses therein have been prepared to scoping level (+-30%). Key Project parameters are presented in Table 3.

Table 3: Summary of Project Parameters

Parameter | Value | Units |

Project Production Rate | Mtpa | 7.0 |

Average Strip Ratio | t/t | 0.016 |

Average FeT Grade in Extracted Tailings | % | 6.8 |

Total Mined Iron | Mt | 7.0 |

LOM | Years | 15 |

Extraction Cost - OPEX | US$/t | 0.65 |

Process Cost - OPEX | US$/t | 1.56 |

Anticipated Average Concentrate Grade | % | 66.8 |

Mining

The Project involves the extraction and reprocessing of the Lac Jeannine tailings based on an extraction rate of 7 Mtpa to produce on average 360 Ktpa of concentrate for 15 years. Based on the study to date, the concentrate is expected to be a premium grade product containing 66.8 % FeT with very low concentrations of deleterious elements such as SiO2, P and Al2O3.

It is anticipated that the rejects from the reprocessing of the tailings will be pumped back into the former Lac Jeannine mine open pit so that the natural topography can, as much as possible, be returned to its natural state.

Whilst the 2026 Inferred Resource is currently restricted to approximately 104 Mt (102.3 Mt is mineable) of material it is recognized that there is additional material present outside of the drill tested area. This material is classified as an exploration target and is presented as a range of grade and tonnes in this PEA study. Any material which is classified as part of the exploration target is treated as waste and stockpiled for the purpose of the 2026 PEA and is not considered as payable material in financial analysis.

The Project design is relatively simple as the tailings pile forms a dome shape with an aerial extent of approximately 1.8 x 1.6 km and an estimated depth of up to 70 m at the central highest point. The 2026 Inferred Mineral Resource is currently restricted to an aerial extent of approximately 1.25 km x 1.40 km with thickness of approximately 50 m to 60 m.

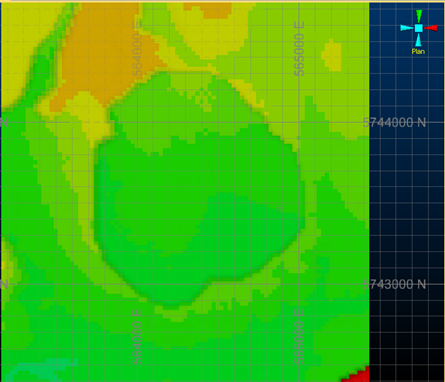

There is a natural gradation in grade from high to low in the tailings pile, which means that the Inferred Resource can be extracted level by level (top to bottom) to eventually form a saucer shaped depression with a depth of up to 60 m from the existing tailings high point and a resultant maximum pit depth of 45 m (Figure 2). Grade variation is observed in the Project schedule as a linear reduction from approximately 8.5% FeT to 7.4 % FeT in the first 3 years of production, grade further reducing to approximately 6.5% FeT by year 10 and subsequently 5.8% FeT in the final year reflecting the vertical variation seen in the Resource block model.

Figure 2: Optimized Pit limits based on Inferred Resources

The maximum extents of the pit were determined through pit optimization of the block model. Each block was allocated an economic value based on the revenue and costs and all blocks with a positive value were sent for processing. The economic breakeven cut-off grade was found to be 3.4 % FeT.

Given there is no surface waste covering (organic material or low grade) it is expected that 100% of the 2026 MRE within the optimized pit limit can be re-processed as the grade of the blocks are all above the economic cut-off grade. The average grade for the Inferred material was 6.8 % FeT.

The proposed mining and material transport method combines a load and carry operation with conveyor-based material transport from the mining area to the concentrator plant. Two front-end loaders excavate the soft, iron-bearing tailings directly at the mining face and carry it over relatively short distances to a belt-feeder hopper. The hopper, mounted on a shiftable bench conveyor, transforms the discontinuous batch feed from the loaders into a continuous material stream for onward conveying to the plant. The bench conveyor can be track-shifted to follow the advance of the mining face: as a mining strip is depleted and the loader travel distances become inefficient, the bench conveyor and hopper are shifted closer to the active mining face.

The deposit is mined bench-by-bench from top to bottom, with bench heights of approx. 5 m to 6 m. Each bench is progressively depleted by radially track-shifting the bench conveyor across the entire deposit area. The head end of the bench conveyor remains fixed near the pit exit, transferring the mined material onto the downstream conveyor towards the concentrator plant. Each track-shift position of the bench conveyor releases a new mining strip for the front-end loaders to excavate.

The average mining rate of 7 Mtpa equates to approximately 1,000 tph to 1,250 tph based on an annual equipment utilization time of 6,500 hours. This can be achieved with two loaders (approx. 9 m³ to 10 m³ buckets each) and a single conveying line, provided the carry distance to the belt feeder hopper stays below 100 m. A Dozer is employed as auxiliary equipment for conveyor track-shifting as well as activities related to pit floor maintenance and bench slope trimming/flattening.

It is expected that the extraction operation can continue throughout the year and material handling issues can be minimized by the rapid turnover of the faces (i.e. prevents permafrost forming). Although the material can become compacted, it is generally relatively dry and self-draining by virtue of the dome shape of the deposit. The digging conditions are not expected to be challenging, but the high silica content will mean that it is highly abrasive.

For the purpose of the 2026 PEA, 2.3 Mt of material that is within the pit limit and is classified as exploration target or waste. The exploration target material will be stockpiled near to the plant. If the exploration material can be shown to be economic through sampling, then it will be processed along with the Inferred material. It was not, however, considered in the 2026 PEA as payable material.

It is also pragmatic to consider the impact on the Project schedule and waste disposal requirements should all of the exploration target material (circa. 40 Mt) be converted to a Mineral Resource. Were this to happen the addition of the exploration target material is unlikely to significantly change the sequence of extraction from a top-down approach, while it will mean the pit can be taken to the extents of the deposit, and this eliminates the formation of the saucer shaped pit.

This will have advantages in terms of slope stability and ease of rehabilitation of the whole of the tailings area. It may also offer potential for an extended period of higher-grade feed in the early years, on the assumption that the higher-grade material seen at the top of the Inferred Mineral Resource extends towards the edge of the tailings. It is envisaged that waste material from the processing facility will be disposed of in the legacy Lac Jeannine open pit. It is estimated there is adequate space present to accommodate processing waste material from both the Mineral Resource and exploration target material.

Capital Costs

Initial CAPEX costs for the Project are based on a ROM of 7 Mtpa with a nominal production capacity of circa. 400 ktpa of 66.8% FeT concentrate. CAPEX costs are estimated at US$69.4M, including EPCM costs and a 15% contingency based on the processing plant and EPCM CAPEX figures.

Sustaining capital over the Project life is estimated at 1.5% of OPEX (excluding G&A) and closure cost is estimated at 5% of total CAPEX, resulting in total life of mine CAPEX cost of US$76.8M.

Table 4: Capital Costs

Description | US$ (M) |

Processing Plant | 44.2 |

Infrastructure | 4.5 |

Extraction | 6.8 |

Indirect Costs (EPCM) | 6.3 |

Estimated Sub-Total Cost | 61.8 |

Contingency 15% | 7.6 |

Sustaining | 3.9 |

Closure cost | 3.5 |

Estimated Total Cost | 76.8 |

Operating Costs

The OPEX includes manpower to run the overall operations, and sub-contracted maintenance teams, power and utilities, materials handling, transport of the concentrate from the Project site to the port and G&A.

Table 5: Operating costs

Area | US$/t ROM | US$/t concentrate |

Tailings extraction (incl. tailings disposal) | 0.65 | 12.46 |

Processing | 1.56 | 29.67 |

Transport all in to port | 0.33 | 6.32 |

G&A | 0.25 |